Author : Nuzzu.S

Date : September 2, 2024

Blockchain Technology Explained in India

Blockchain technology is often heralded as one of the most transformative innovations of the 21st century, with the potential to revolutionize industries from finance to supply chain[1] management. In India, the interest in blockchain has surged over recent years, making it a key area of exploration and investment. But what exactly is blockchain, and how is it being utilized in India? This article delves into the world of blockchain, explaining its workings, applications, and future potential in India.

History and Evolution of Blockchain

Early Developments in Blockchain Technology

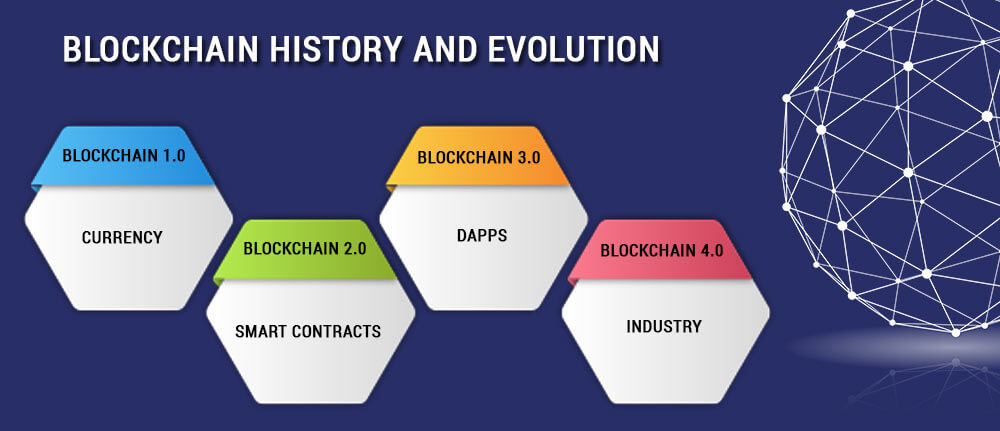

Blockchain technology began with the creation of Bitcoin in 2008 by an anonymous entity known as Satoshi Nakamoto. Initially, blockchain was simply the technology underlying Bitcoin[1], a digital currency that promised to disrupt traditional banking by enabling peer-to-peer transactions without intermediaries.

Key Milestones in Blockchain Adoption Worldwide

Since its inception, blockchain has grown beyond cryptocurrencies. The technology has found applications in various sectors, including finance, healthcare, and supply chains. Countries like the USA, Japan, and China have led in blockchain adoption, setting the stage for a global blockchain revolution.

Blockchain’s Entry into India

India’s tryst with blockchain began in the early 2010s, primarily driven by the need for transparency in financial transactions and government services[2]. With a large population and a growing digital economy, India presents fertile ground for blockchain innovation.

How Blockchain Technology Works

Basic Structure of a Blockchain

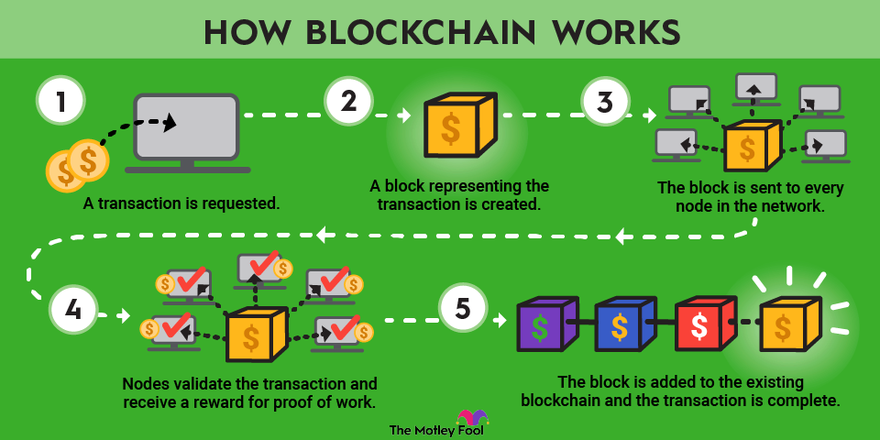

At its core, a blockchain is a decentralized digital ledger that records transactions across multiple computers in such a way that the registered transactions cannot be altered retroactively. Each block in the chain lists transactions, and the system records every new transaction in a fresh block.

The Role of Cryptography in Blockchain

Cryptography is the backbone of blockchain technology, ensuring the security and integrity of data. Through techniques like hashing and digital signatures, blockchain ensures that once a transaction is recorded, it is immutable and transparent to all participants in the network.

Types of Blockchains: Public vs. Private

There are different types of blockchains—public and private. Public blockchains, like Bitcoin and Ethereum, are open to anyone and are highly decentralized. Private blockchains, on the other hand, are controlled by a specific organization and are often used in enterprise settings where privacy is paramount.

Applications of Blockchain in India

Financial Sector

Cryptocurrency and Blockchain in Banking

In the financial sector, blockchain has brought about significant changes, especially with the introduction of cryptocurrencies. Despite the regulatory uncertainty, cryptocurrencies like Bitcoin and Ethereum have gained popularity in India, with many financial institutions[3] exploring blockchain for secure and efficient banking solutions

Use of Blockchain in Payment Systems

Blockchain is also being explored for its potential to revolutionize payment systems in India. With initiatives like the Unified Payments Interface (UPI) already transforming digital payments, blockchain could further enhance security and reduce transaction costs.

Government and Public Services

Land Registration and Property Rights

One of the most promising applications of blockchain in India is in land registration and property rights. The immutability of blockchain records makes it an ideal solution for eliminating land disputes, ensuring transparency, and reducing fraud in property transactions.

Digital Identity and Blockchain

The Indian government is also exploring blockchain for digital identity solutions[4]. With the Aadhaar system already in place, blockchain could provide an additional layer of security and privacy, ensuring that personal data is protected from breaches and misuse.

Supply Chain Management

Enhancing Transparency in Supply Chains

India’s vast and complex supply chains, especially in agriculture, can benefit greatly from blockchain technology. By providing a transparent and traceable record of goods from production to sale, blockchain can help reduce fraud, improve efficiency, and ensure the quality of products.

Blockchain in Agriculture and Food Safety

In the agricultural sector, blockchain can be used to track the origin and quality of food products, ensuring that consumers receive safe and authentic goods. This is particularly important in a country like India, where agriculture plays a crucial role in the economy.

Blockchain Regulations in India

Government’s Stance on Blockchain

The Indian government has shown interest in blockchain technology, recognizing its potential to improve governance and economic efficiency. However, the government remains cautious, especially regarding cryptocurrencies, which have faced regulatory hurdles.

Regulatory Framework for Cryptocurrencies

In recent years, the Indian government has taken steps to regulate cryptocurrencies, banning their use in certain contexts while also exploring the possibility of a central bank digital currency (CBDC). The future of cryptocurrencies in India remains uncertain, with ongoing debates about their legality and regulation.

Future Legal Developments

As blockchain technology continues to evolve, so too will the legal frameworks governing it. India is expected to develop more comprehensive regulations that will enable the growth of blockchain while addressing concerns around security and privacy.

Challenges Facing Blockchain Adoption in India

Technical Challenges

Blockchain technology, while promising, faces several technical challenges in India. These include scalability issues, energy consumption, and the need for robust infrastructure to support widespread adoption.

Regulatory and Legal Challenges

The regulatory landscape for blockchain in India is still evolving, with uncertainties around the legal status of cryptocurrencies and other blockchain applications. Navigating this complex environment remains a significant challenge for businesses and developers.

Public Awareness and Education

One of the biggest barriers to blockchain adoption in India is the lack of awareness and education. Many people, including business leaders and policymakers, are still unfamiliar with how blockchain works and its potential benefits, which hinders widespread adoption.

Future of Blockchain in India

Potential for Growth and Innovation

Despite the challenges, the future of blockchain in India looks promising. With a growing number of startups and tech companies exploring blockchain applications, there is significant potential for innovation and economic growth.

The Role of Startups and Tech Giants

Startups and tech giants alike are playing a crucial role in driving blockchain adoption in India. From fintech to supply chain management, these companies are developing new solutions that leverage blockchain technology to address real-world problems.

Blockchain’s Potential to Transform Indian Society

In the long term, blockchain has the potential to transform Indian society by improving transparency, reducing corruption, and enhancing the efficiency of various systems. Whether in government services[5], financial transactions, or supply chains, blockchain could play a key role in India’s digital future.

Conclusion

Blockchain technology offers immense potential for India, from revolutionizing the financial sector to enhancing the transparency of government services. While challenges remain, the continued exploration and adoption of blockchain could position India as a leader in this emerging field. As the technology matures and regulatory frameworks evolve, blockchain could become a cornerstone of India’s digital economy, driving innovation and economic growth for years to come.

FAQs

What is the Future of Blockchain in India? The future of blockchain in India is promising, with potential growth in various sectors, driven by startups and tech giants, despite the existing challenges.

What is blockchain technology? Blockchain is a decentralized digital ledger that records transactions across multiple computers. It ensures that the data is immutable and transparent.

How is blockchain being used in India? Blockchain is being used in various sectors in India, including finance, government services, and supply chain management, to enhance transparency and efficiency.

What Are the Benefits of Blockchain? The benefits of blockchain include increased transparency, improved security, reduced costs, and the elimination of intermediaries in transactions.

What Are the Challenges of Blockchain Adoption in India? Challenges include technical limitations, regulatory uncertainties, and a lack of public awareness and education about blockchain technology.